Gordon growth model is a variant of the Discounted cash flow model, a method for valuing a stock or business. Often used to provide difficult-to-resolve valuation issues for litigation, tax planning, and business transactions that are currently off market. It is named after Myron Gordon, who was a professor at the University of Toronto.

It assumes that the company issues a dividend that has a current value of D that grows at a constant rate g. It also assumes that the required rate of return for the stock remains constant at k which is equal to the cost of equity for that company. It involves summing the infinite series which gives the value of price current P.

.

.

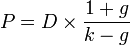

Summing the infinite series we get,

, In practice this P is then adjusted by various factors e.g. the size of the company.

, In practice this P is then adjusted by various factors e.g. the size of the company. , k denotes expected return = yield + expected growth.

, k denotes expected return = yield + expected growth.

It is common to use the next value of D given by D1 = D0(1 + g), thus the Gordon's model can be stated as [1]

.

.

Note that the model assumes that the earnings growth is constant for perpetuity. In practice a very high growth rate cannot be sustained for a long time. Often it is assumed that the high growth rate can be sustained for only a limited number of years. After that only a sustainable growth rate will be experienced. This corresponds to the terminal case of the Discounted cash flow model. Gordon's model is thus applicable to the terminal case.

No comments:

Post a Comment